The Avocado Export Boom — Who Actually Eats Them?

A Murang'a farmer's avocados are on a Berlin shelf this morning.

His grandson, in Murang'a, has not eaten one this season.

Kenya's avocado export boom is the success story of the last decade in Kenyan agriculture. We are now Africa's largest exporter of fresh avocados. The numbers are real: over 100,000 tonnes a year shipped to Europe, China, and the Middle East. Smallholder incomes in some avocado-growing counties have doubled. The crop has fed school fees, built houses, paid hospital bills.

It is also a story with a quiet asymmetry. The fruit travels. The nutrition stays — but mostly with the people who can buy it back at the export-pegged retail price.

Let's hold the boom and the asymmetry in the same hand.

Table of Contents

- The Numbers, Briefly

- The Margin Problem

- What's Lost

- What's Gained

- What Better Policy Would Do

- Why I Wrote This

The Numbers, Briefly

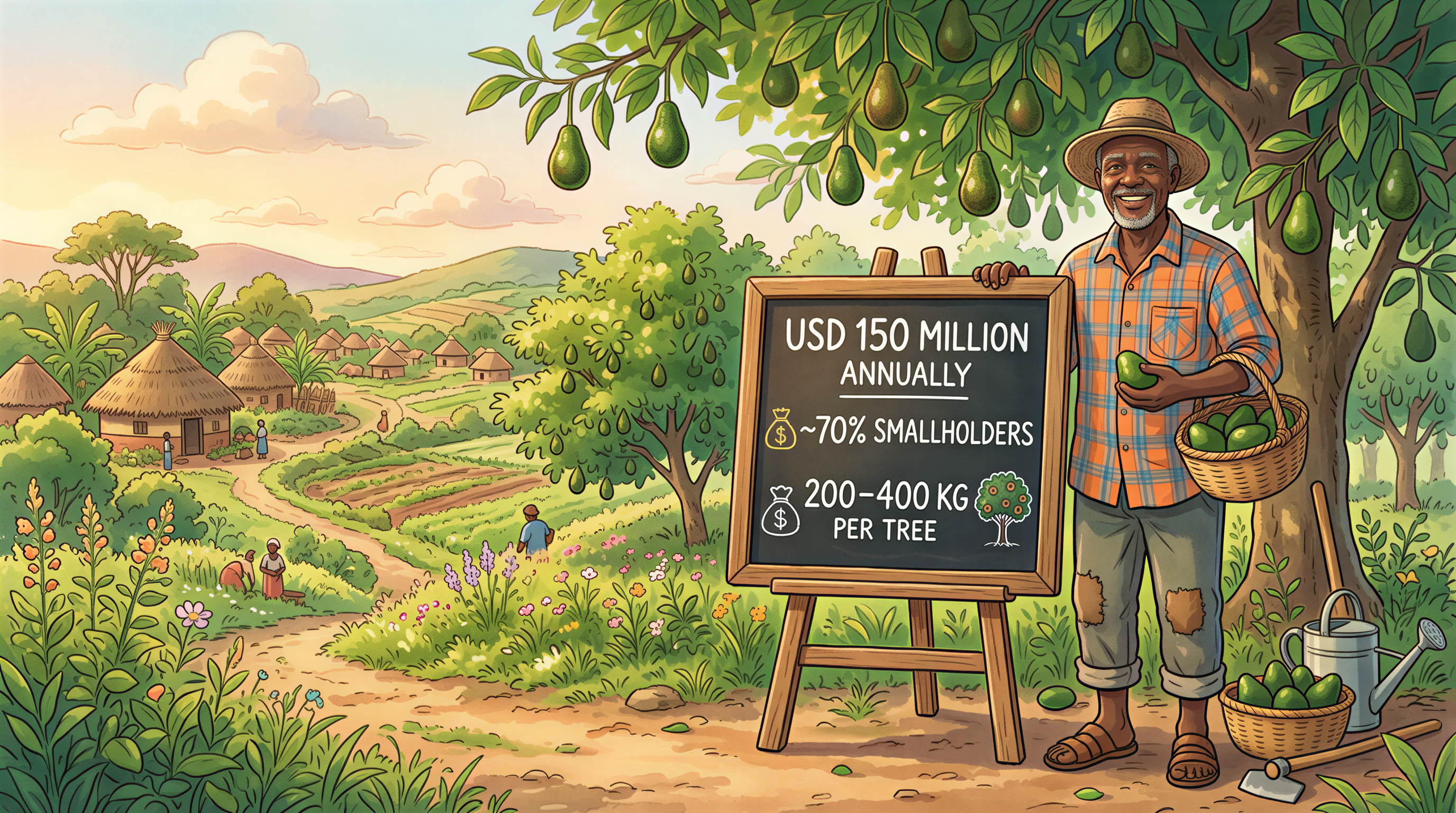

Kenya's avocado export industry has grown from negligible in the early 2000s to over USD 150 million a year by 2024. Most of the production is from smallholder farmers — about 70% of the export crop comes from farms under two hectares. The varieties are predominantly Hass and Fuerte. The destinations are predominantly the EU and, increasingly, China.

For the smallholder farmer, the income is real. A productive Hass tree can yield 200–400 kg a year. At export-grade prices, that's KSh 30,000–80,000 per tree per year, before broker margins. A farm with thirty productive trees is generating real cash flow that did not exist twenty years ago.

This is the success. We should celebrate it.

The next paragraph is the part we celebrate less.

The Margin Problem

A Murang'a smallholder selling to an export aggregator typically receives KSh 25–45 per kilo at the farm gate. That same kilo retails on a Berlin shelf for the equivalent of KSh 600–1,000.

The intermediation chain — aggregator, exporter, importer, retailer — captures roughly 90% of the final retail value. Some of that is real cost (cold-chain logistics, shipping, ripening, distribution). Some of it is margin from market position.

In Nairobi supermarkets, an export-grade Hass avocado costs KSh 80–150 in season — pegged to export prices, not local production cost. A bag of "lower-grade" or rejected avocados at sokoni costs much less, but those are increasingly being absorbed by export aggregators too, sometimes for cosmetic export, sometimes for processing into oil or pulp for export markets.

The result: avocados grown in Kenya, by Kenyans, are increasingly priced for non-Kenyan stomachs. The fruit is on the shelf. The price is at the boundary.

What's Lost

Three things, each meaningful.

1. The most nutrient-dense fruit available in Kenya is becoming a luxury item locally.

Avocados are unusually nutrient-dense — monounsaturated fats, fibre, potassium, folate, vitamin K. For Kenyan children and pregnant mothers, they are an exceptionally cheap and dense form of healthy fat. As the price rises, the in-country consumption pattern shifts toward higher-income households, exactly the households that need the nutrients least.

We have engineered a public-health regression in slow motion.

2. Smallholder children are eating less of what their family grows.

This is the bit that surprises people. Many smallholder avocado farmers send virtually their entire harvest to brokers. The household keeps the rejects (split, oversize, blemished) and the late-season fall-offs. The farm-family child of a Murang'a avocado grower may eat fewer avocados in a year than a middle-class Nairobi child.

This is not because the family is cruel. It is because the export price relative to the household budget makes "selling and buying back" mathematically irrational. Eat one fruit at home, lose KSh 80 of cash that the household needs for school fees.

3. The local market is being hollowed out.

In counties without strong local market infrastructure, the export aggregator is often the only buyer. This means the farmer cannot diversify destinations. If export prices crash (as they did briefly in 2021–22 due to oversupply and shipping disruption), the farmer has no fallback market. The local market that could have absorbed surplus has already shrunk.

This is a fragility we did not have when the trade was smaller.

What's Gained

Let me steelman the other side.

The export boom has done four real things:

1. Income. Smallholder cash flow is materially higher. School completion rates in avocado-producing wards have risen. Real numbers, real lives.

2. Investment. Some of that cash flow is reinvested in better planting material, better post-harvest, irrigation, and crop diversification. The next generation of avocado farms are more productive than the first.

3. National foreign exchange. Avocados earn dollars. Dollars stabilise the shilling. The macro effect is small but positive.

4. Aspirational signal. The story of "smallholder farmer feeds Berlin breakfast" is morale-shaping. Kenyan agriculture has too few such stories.

Anyone who tells you the boom is purely extractive is wrong. It is genuinely net-positive for many farmers. The asymmetry is real and the gains are real.

The question is what we do with the asymmetry.

What Better Policy Would Do

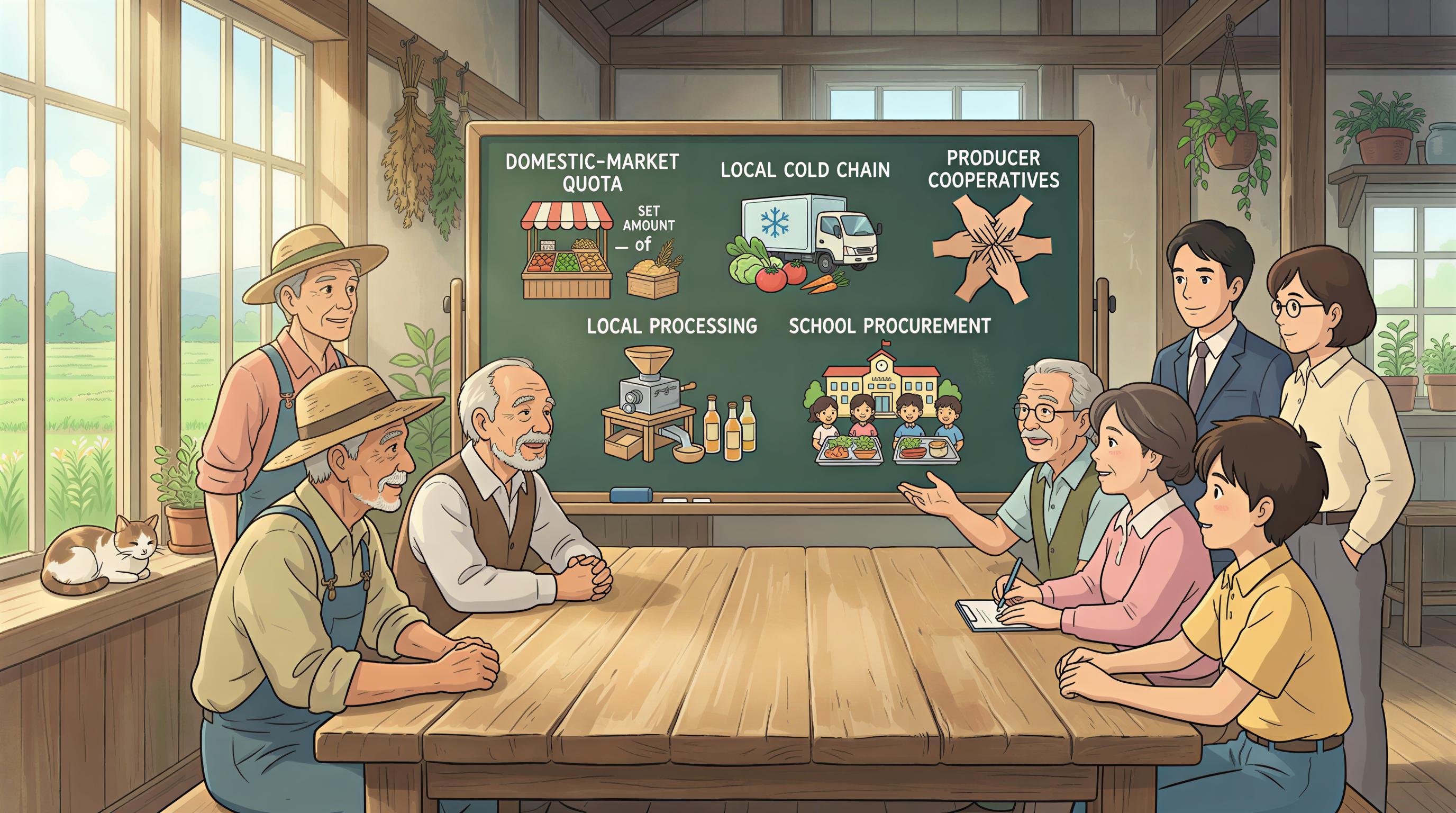

Five steps. Each modest. Combined, transformative.

1. Mandate a domestic-market quota.

Senegal does this with peanuts. Côte d'Ivoire does it with cashews in some forms. A simple rule: 15–20% of any export aggregator's volume must be sold into the domestic market at controlled-margin prices. This keeps a meaningful supply at non-export prices for Kenyan consumers.

2. Invest in local cold chain.

A working cold chain extending from farm gate to local market would let smallholders bypass the export aggregator on a portion of their harvest. The infrastructure cost is real but smaller than most agricultural mega-projects.

3. Strengthen producer cooperatives.

A cooperative bargaining at scale captures more of the export margin for the smallholder. Where cooperatives have been organised — like in some Murang'a, Meru, and Embu wards — farm-gate prices are 30–40% higher than where they have not.

4. Local processing for added value.

Avocado oil, pulp, dehydrated products. Currently almost all processing happens in Europe. Capturing even a fraction in-country increases retained value, creates rural jobs, and produces a market for second-grade fruit that currently goes to waste.

5. School and clinic procurement.

A government procurement programme that buys a small slice of the harvest for school feeding programmes and ANC clinics — at locally-negotiated prices — would do double duty: stabilise farmer income and improve child and maternal nutrition.

This is not industrial policy nostalgia. It is sensible market design.

Why I Wrote This

Because the celebration version of the avocado boom is the only version most policy conversations engage with. The asymmetry version — the one a Murang'a child lives — is the one that should be shaping the next stage of policy.

I am not anti-export. I am anti-extractive structures sold as success stories. The boom is good. It can be much better.

For the related conversation on what Kenyan food sovereignty should mean, see the price of a plate and traditional foods, modern nutrition.

The fruit grew here. Some of it should stay.